The Brief History of Accounting [Notes with PDF]

What is the brief history of accounting?

If you want to learn something thoroughly, you must first learn about its past history. History provides a complete picture of every situation.

So, if you want to understand how accounting has evolved and arrived at this stage, you must first understand accounting’s history.

As a result, in this post, we will learn a brief history of accounting so that you can quickly grasp and understand the history of accounting.

Accounting has a history that is as old as human civilization. So it can be said that the origin of accounting is from the dawn of human civilization.

Accounting has evolved to its present state as a result of evolution and demand.

From the beginning of time until now, when the world’s civilization has developed and the method of production, trade and distribution of goods has been implemented, the accounting system has been introduced in its own unique way and context.

It is thought that sometime around 1340, accounting was introduced between the ancient Chinese civilization, the Babylonian civilization, the Indian civilization, and the Egyptian civilization.

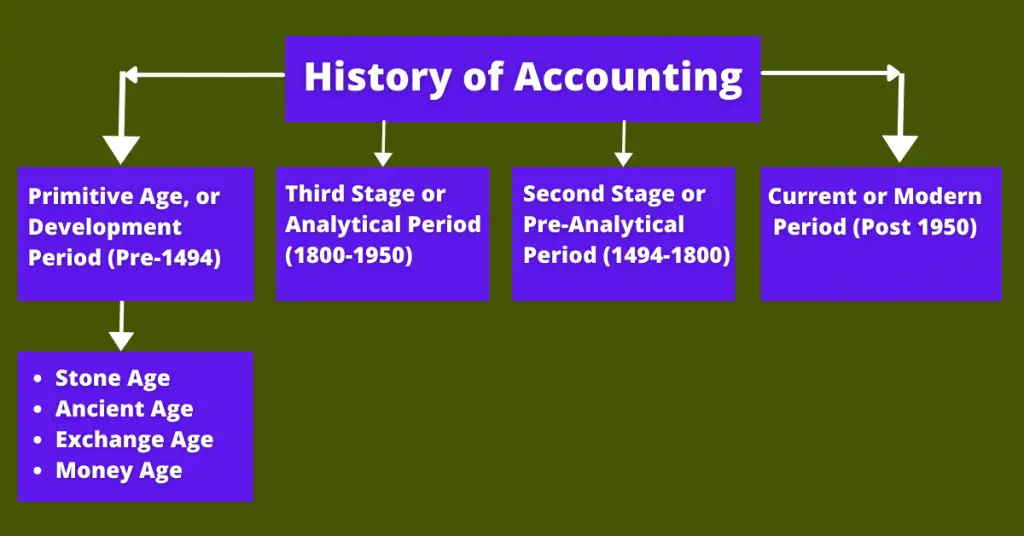

The origin and evolution of accounting have been divided into four stages:

- Primitive Age, or Development Period (Pre-1494)

- Second Stage, or Pre-Analytical Period (1494-1800)

- Third Stage, or Analytical Period (1800-1950)

- Current or Modern Period (Post 1950)

The graphical presentation of the brief history of accounting is as follows:

1.Primitive Age or Development Period (Pre-1494):

The period from the dawn of civilization to 1494 has been classified as the development period or primitive age.

The era is further divided into four parts depending on the type of accounting system in use at the time:

- Stone Age

- Ancient Age

- Exchange Age

- Money Age

Stone Age:

People lived in the Stone Age by hunting animals and eating tree fruits.

People used to live in forests and mountain caves. Inside the cave, they collected the necessary food and carved it on the cave, or by drawing pictures or making marks on the rocks, to keep track of the number of fruits collected and the number of prey.

Basically, the foundation of accounting was laid from this calculation.

Ancient Age:

People left caves in the mountains and began living in a socialized environment in ancient times. As society grew, they did social work, farming, and other economic activities.

People used to cut the marks on the walls of their houses and tie the knots on the ropes, cut the marks on the bamboo, and save the accounts of their crops and livestock during this time period.

Exchange Age:

People began to adopt various occupations to earn a living as society evolved and the scope of human economic activities expanded.

Some chose farming as a profession, while others chose hunting or animal husbandry. The farmer requires meat, and the hunter requires grain. As a result, trade in goods began.

The exchange of goods marks a new milestone in the accounting process. This exchange was once saved by painting on earthen walls or carving on wooden doors.

In China at the time, a type of instrument known as an abacus was used in accounting.

Money Age:

During the money age, the calculation of goods exchange was based on quantity theory. This would have resulted in a number of complications.

The currency system was introduced with the common will of all to overcome the difficulties of the exchange system.

During the hunting era, leather was used as currency. The professional merchant class did not emerge until after the invention of currency, and the currency was introduced as a medium of exchange.

Cowrie, on the other hand, was used as a means of transaction settlement in India prior to the introduction of currency.

2. Second Stage or Pre-Analytical Period (1494-1800):

The period from 1494 to 1800 is considered the Pre-Analytical Period. At the beginning of this century, trade flourished in the Italian port of Genoa.

With the expansion of trade and commerce comes the complexity of business trade and the need to apply specific policies in accounting.

Finally, in 1494, Luca Pacioli, a priest, and mathematician published a groundbreaking book “Summa de Arithmetica Geometrica, Proportione et Proportionalita” on the double-entry accounting system.

The current accounting system is being introduced based on this double-entry accounting system.

In the last chapter of this book, he discovered the basic method of accounting or the formula for determining the debit credit of a transaction.

3. Third Stage or Analytical Period (1800-1950):

The period from 1800 to 1950 is considered the analysis phase. At this time the rationality of the working of the accountants was analyzed.

Large-scale production processes, factory production systems, the emergence of joint venture companies, and huge competition have led to many complications in accounting, such as declining product prices and huge profits.

As a result, accounting research was started to solve these problems and new theories were discovered. Basically, the path of modern accounting started from this era.

4. Current or Modern Period (Post 1950):

The beginning of the modern era of accounting is basically from the middle of the twentieth century. During this time great changes took place in accounting.

It was in this century that accounting was compared to information systems. After the Second World War, with the advancement of science and technology came the advancement of industry and commerce.

The scope of accounting activities increases. In the changed situation, accounting is in great demand for information and various stakeholders are starting to rely on accounting for information.

Significant development of accounting at this time was:

- The emergence of accounting standards and

- The emergence of various branches of accounting.

Conclusion

Therefore, it can be said that in the current socio-economic context and with the evolution of business, accounting has evolved and this trend is expected to continue.

You can also read:

- Top 10 Objectives of Accounting

- How does Accounting Create Value and Accountability

- What is the Importance of Accounting